April 9, 2025

Written by: Izzy Rosenzweig

Founder & CEO, Portless

Izzy is the Founder and CEO of Portless, an Ecommerce fulfillment expert with 10+ years’ experience helping brands streamline global supply chains, accelerate cash flow, and scale DTC operations. Izzy frequently speaks on supply chain innovation and cross-border logistics.

LinkedIn|Twitter

Disclaimer: this blog post is not legal advice and is for informational purposes only. Please seek guidance from your own legal counsel before utilizing any information you see here.

Brands using a direct supply chain model can strategically appraise their goods for US tariffsusing established transaction value methodologies.

With the recent announcement of worldwide tariffs on goods being imported into the United States, many ecommerce merchants are wondering how to appraise their goods

Traditional supply chain vs. Direct supply chain

How direct supply chain merchants should appraise their goods

How does that differ from the “First Sale” methodology?

How Portless enables ecommerce merchants to defer their tariffs

Section 1: Traditional supply chain vs. Direct supply chain

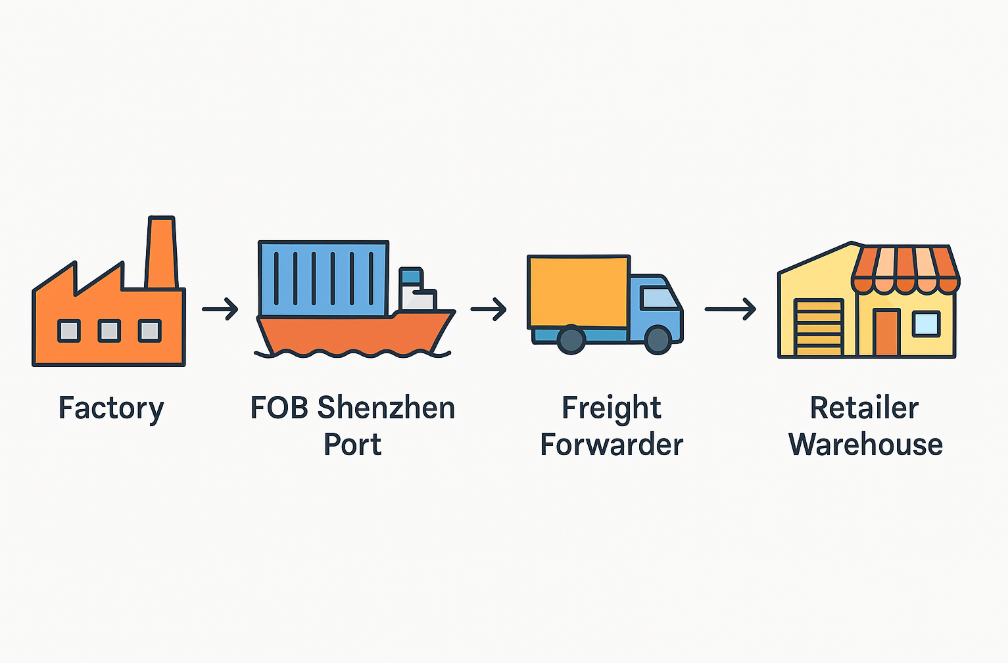

In a traditional supply chain model, a retailer buys merchandise from a factory overseas. The retailer typically buys the merchandise “FOB [Port City X]” (for example, FOB Shenzhen Port), meaning the factory is responsible for delivering the goods in a shipping container “Free on Board” to the Shenzhen Port. The retailer would then work with a freight forwarding company to import the shipping container into the US. 6-8 weeks later, the container would arrive at the retailer’s warehouse or 3PL and the goods would become available for sale.

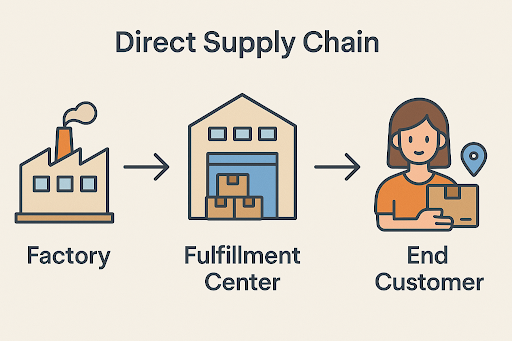

In a direct supply chain model, such as the one employedlike those used by Shein, Temu, and brands leveraging...

Section 2: How direct supply chain merchants should appraise their goods

In a traditional supply chain model, the importer uses the “transaction value” - the amount actually paid to the factory for the goods - as the appraisal price.

What about in a direct supply chain model, where the Ecommerce merchant has already sold the goods to an end consumer prior to the importation?

The key advantage for direct supply chain merchants: the merchant can still use the transaction value, i.e. the amount they paid the factory for the goods.

Why?

All merchandise imported into the United States must be “appraised” in accordance with .S.C. § 1401a).

And here is the key: there is a presumption by CBP (U.S. Customs and Border Protection)

Therefore, as long as the ecommerce merchant or an entity acting on their behalf is listed as the importer of record, the fact that there is an additional sale to an ultimate consignee (the end customer) is irrelevant; CBP cares about the value the importer paid for the goods, not the price at which they ultimately sold the goods.

Please note that it is important to use a reputable fulfillment center that understands these rules, as there are some additional complexities (like ensuring that the original sale was “for exportation to the United States”) that can trip you up if you are not careful. In particular, using the correct Importer of Record is critical to getting this right with U.S. Customs and Border Protection.

For additional clarity, here is a clip of Portless CEO Izzy Rosenzweig and Lenny Feldman discussing this on our recent tariffs-focused webinar. Lenny is a Principal at Sandler, Travis & Rosenberg and one of the nation's leading experts on import and export compliance, having served on the Commercial Customs Operations Advisory Committee (COAC) for U.S. Customs and Border Protection — appointed by three different Secretaries of the Treasury.

(Want to see the full webinar recording? Sign up here >>)

Section 3: How does this differ from the “First Sale” methodology?

For almost all merchants, using transaction value is sufficient; this allows them to use the price they actually paid their factory for their goods as the appraised value for US tariffs.

However, in certain unique instances, merchants can take advantage of the “First Sale” methodology to pay tariffs on a value even lower than the standard transaction value.

This methodology works through a specific legal framework:

In 1988, the U.S. Court of Appeals for the Federal Circuit decided the case ofE.C. McAfee Co. v. United States, which established the "first sale" rule in U.S. import law. This rule allows importers to base the dutiable value of merchandise on the price paid in the initial sale, typically between the manufacturer and a middleman, rather than the price paid by the importer to the middleman. This can result in significant duty savings. The middleman can sometimes be a third party but is often a secondary entity (such as a Hong Kong corporation) set up by the factory itself for expressly this purpose.

Len Rosenberg, a senior attorney at Sandler, Travis & Rosenberg, P.A. (the same firm as Lenny Feldman from our webinar!), represented E.C. McAfee Co. in this landmark case. The court held that the price paid by the middleman to the manufacturer was the proper basis for transaction value, provided that the transaction was conducted at arm's length and involved goods clearly destined for export to the United States.

In other words, if there are multiple sales between the factory and the importer, the importer is allowed to use the value of the “First Sale”.This enables the importer to shift ~10-20% of the costs of the item (typically costs unrelated to manufacturing, like marketing, finance, etc.) to a middleman, and reduces their dutiable rate accordingly.

Importantly, this is generally only relevant for larger merchants that are buying significant quantities of goods from a single factory. Setting up a proper first sale methodology requires expert guidance from tax professionals. The 10-20% savings on tariffs would generally not pay for the overhead of running a proper First Sale program unless a merchant is buying $1-2M of goods from a single factory annually.

[1]

Section 4: How Portless enables ecommerce merchants to defer their tariffs

Merchants leveraging Portless's fulfillment model gain significant operational benefits compared to traditional models.

In a traditional supply chain, the merchant pays tariffs on the entire container the minute it enters the US - even if they don’t sell the goods for weeks, months, or ever! With the current tariffs, that could easily be tens of thousands of dollars paid upfront.

But by using Portless, tariff deferment is naturally baked in; the tariff is only due once the item is already sold. This way, tariffs are deferred until there is enough cash to pay for them, and the merchant never needs to pay tariffs on slow or unsold inventory.

In addition to tariff deferment, Portless has been working on other methods to support our brands and reduce complexity. In our merchant portal, we now have a way to easily comply with U.S. Customs and Border Protection data requirements, including:

HS code recommendations

Suggested product descriptions

Automatic tariff calculations

Q: What is a tariff in simple terms?

A: A tariff is a tax a country charges on goods that are imported from another country. We use them to collect revenue and to protect local industries, since tariffs make imported goods cost more.

Q: How do I defer tariffs when selling online?

A: I can defer tariffs by using a direct supply chain. That means I store goods in a fulfillment center overseas, only import them once the items sell, and pay duty at that point. This spreads out my costs, so I’m not paying tariffs on products that haven't sold yet.

Q: How can Portless help my brand hold off paying tariffs until after a sale?

A: We partner with brands to ship items from a fulfillment center overseas to the shopper only when the item sells. This way, tariffs are due on a per-order basis instead of all at once. That saves cash flow and prevents me from paying tariffs on inventory I haven’t sold.