Most DTC brands treat international expansion the same way: interesting in theory, too complicated in practice. The objections are familiar. Customs is a headache. Returns are a nightmare. Setting up a new warehouse in every market? Even worse. What if we launch in a new market and have to pull back?

So they don’t expand. And every day they don’t, international customers who want their products buy from someone else — or don’t buy at all.

The cross-border Ecommerce market is projected to grow at roughly 15% annually through 2034. According to a 2025 study of 100 senior Ecommerce leaders, 91% say international sales are profitable, and nearly half generate 20% or more of total revenue from global markets. The demand is there. The question is whether your fulfillment model can serve it.

The fear is that international expansion is a big, risky bet. The data says otherwise.

We analyzed a sample of 89 merchants on the Portless platform to track what happens after brands start shipping internationally. The pattern is consistent: expansion isn’t a one-time gamble. It’s a gradual, self-reinforcing process that accelerates over time and is fueled by your supply chain management.

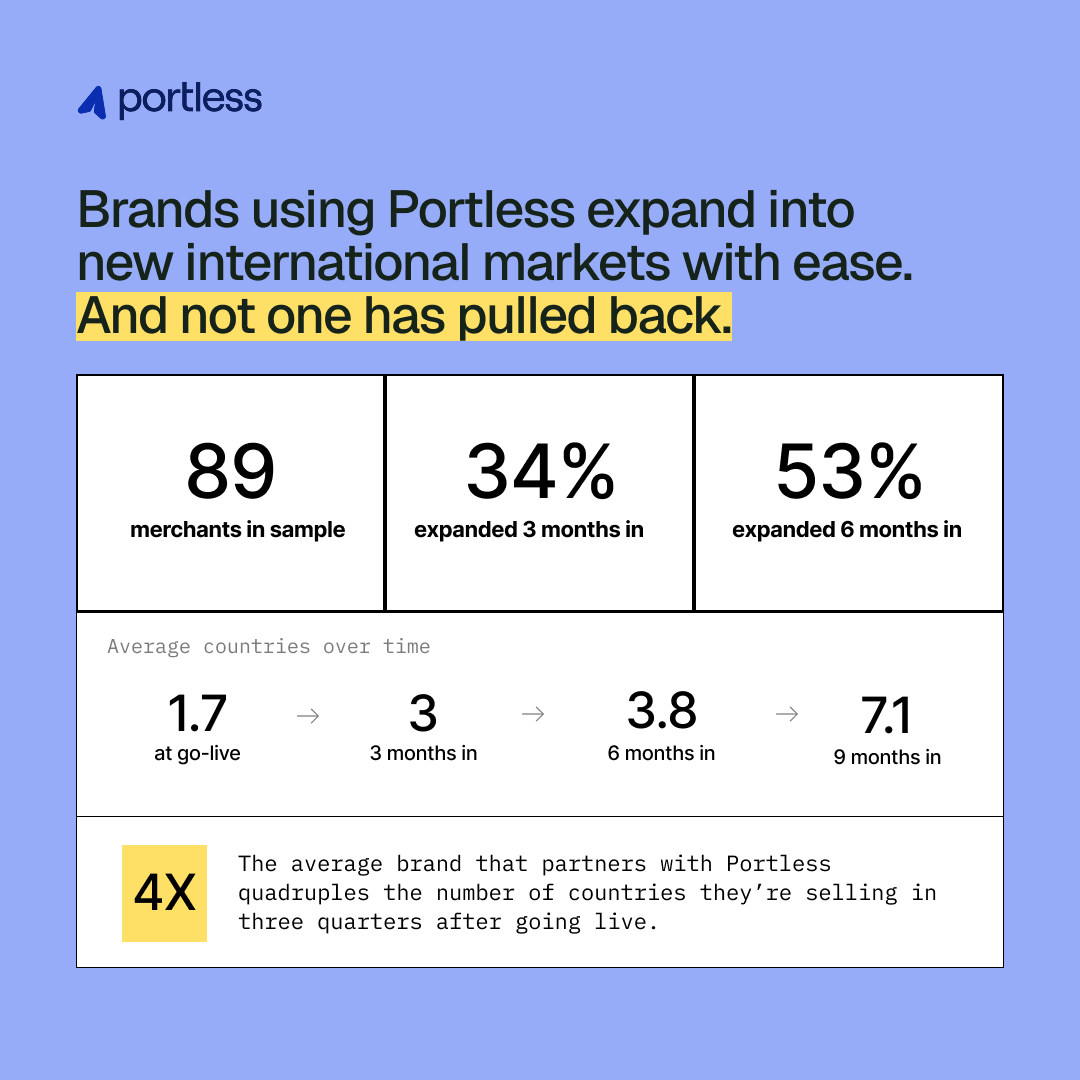

34% of brands expanded into new countries within their first three months of going live with Portless. By six months, 53% had added at least one new market. And the average brand quadrupled its country count — from 1.7 to 7.1 — within nine months.

This isn’t a story about brands taking a risk and getting lucky. It’s a pattern: once the infrastructure barrier is removed, expansion happens on its own. Brands test a market, see traction, and add another. The risk profile is closer to running a new ad campaign than opening a new warehouse.

Darwish Gani, founder of OpenBorder, talked about how to test a new market on The Modern Supply Chain podcast:

The reason most brands write off international expansion isn’t that the markets aren’t there. It’s that their fulfillment model makes expansion genuinely expensive and operationally complex.

Under the legacy 3PL model, expanding to a new region means standing up new infrastructure: a warehouse lease, inventory pre-positioning, local carrier contracts, and customs brokerage. A conservative estimate for a single new region is $50,000+ in setup and initial inventory commitment — before you’ve sold a single unit.

That’s not a test. That’s a bet. And for a growing DTC brand doing $2–5M in revenue, it’s a bet that competes directly with product development, marketing, and hiring.

Pre-positioning inventory in a new market means forecasting demand in a region you’ve never sold in. You’re guessing how many units to ship, which SKUs to stock, and how much safety stock to carry — all with zero historical data. Get it wrong and you’re sitting on dead inventory in a market that hasn’t proven itself.

Pulling back is expensive too. If a market doesn’t work, you’ve already sunk the warehouse setup costs, shipped the inventory, and committed to carrier contracts. The legacy model punishes experimentation. So brands don’t experiment — they wait until they’re “sure,” which often means they never start.

The reason the 89 merchants in our dataset expanded so quickly isn’t that they’re uniquely bold. It’s that direct fulfillment from China removes the per-region infrastructure cost that makes expansion feel risky under the legacy model.

With direct fulfillment, you ship from a single inventory pool to 75+ countries. There’s no warehouse to set up in each market. No inventory to pre-position. No carrier contracts to negotiate per region. You’re selling the same inventory to Australia, the UK, Germany, and Japan — without duplicating your supply chain for each one.

That changes the math on experimentation entirely. Testing a new market doesn’t cost $50,000. It costs whatever you spend on ads to drive traffic. If the market works, you scale it. If it doesn’t, you haven’t committed anything.

Craft Club is a good example. The Australian craft kit brand was managing inventory across three warehouses and hitting revenue ceilings because all their cash was tied up in production and ocean freight. After switching to direct fulfillment with Portless, they consolidated to a single fulfillment center in Shenzhen and started shipping globally from one inventory pool. They eliminated the complexity of balancing stock across multiple warehouses and markets, and grew 300% — with no limiting factors on continued expansion.

The warehouse decision is just one part of your broader Ecommerce fulfillment model. But it’s the part that determines whether international expansion is a $50K bet or a low-risk experiment. For a deeper look at building an international growth plan, see our guide to international Ecommerce strategy.

The brands losing international customers aren’t losing because demand isn’t there. They’re losing because their fulfillment model makes expansion feel impossible when it doesn’t have to be. The infrastructure barrier is real under the legacy model — but it’s not the only model. Talk to our team to see what international expansion looks like when you remove the warehouse from the equation.

There’s no per-region setup cost. You ship from a single inventory pool to 75+ countries, so expanding to a new market costs whatever you spend to acquire customers there — not the $50,000+ in warehouse infrastructure that legacy 3PLs require.

No. Direct fulfillment ships from one location to customers worldwide. You don’t pre-position inventory in each market, which eliminates the forecasting risk and capital commitment that makes traditional international expansion expensive.

You pull back with zero sunk infrastructure cost. Because you haven’t set up a warehouse or pre-positioned inventory, there’s nothing to unwind. This is the fundamental difference from the 3PL model, where pulling back means writing off setup costs and unsold inventory.

Portless ships to 75+ countries from fulfillment centers in China. You serve all of them from a single inventory pool — no per-region warehouse setup required.

Based on data from 89 merchants, 34% expand into new countries within three months and 53% within six months. The average brand quadruples its country count from 1.7 to 7.1 within nine months of going live.